Net Zero – Where are we?

Net zero has a guilty reputation for feeling like a vast and often complicated topic. Even so, it remains a topic that the entire global real estate and construction industry are deeply engaged in.

The mix in terminologies used and various targets set have been difficult to follow, so it’s understandable that the industry, with contrasting perspectives, find it challenging to collaboratively navigate.

One thing that UK’s built environment community commonly agrees on, is the need for a united framework to reduce ambiguity. Enter the UK Net Zero Carbon Buildings Standard, supported by a coalition of professionals.

The standard is crucially underpinned by an evidence-based reporting methodology. Measuring in-use data rather than theoretical models, with the aim to drive accountability and hopefully prevent greenwashing.

Brookbanks embraces these aims and welcomes the standard, which plans to move from pilot phase to implementation in late 2025. But what other factors will drive net zero forward in the UK beyond regulatory compliance? Brookbanks want to briefly explore in this thought piece.

Firstly, a quick look at some of the milestone points of net zero’s journey so far and definitions of the language commonly used.

Brief history lesson…

The concept of net zero has come a long way in a short space of time. Some of the significant dates:

- 2009 – Scientists publish a paper regarding global warming

- 2014 – IPCC Fifth Assessment Report (limiting global temperature change means limiting C02 emissions to the atmosphere)

- 2015 – The Paris Agreement (A turning point in efforts to tackle climate change)

- 2017 – Sweden become first to enshrine net zero by 2045 into Law

- 2018 – IPCC makes 1.5◦C link and the mid-20th century necessary target

- 2019 – UK become 1st G7 country to legislate net zero by 2050

To achieve a safe and habitable planet, climate science shows that the average global temperature rise needs to be limited to 1.5°C above pre-industrial levels. To limit global temperature rises and mitigate climate change the UK has committed to reaching net zero by 2050.

This means that the total greenhouse gas emissions would be equal to the emissions removed from the atmosphere.

So, (NZC = EE ≤ ER) – A positive strategy providing clearer aims to foster early adoption.

The UK Government has developed a suite of policies in order to reach net zero, set out in two strategy publications: the Net Zero Strategy (2021) and Powering Up Britain: The Net Zero Growth Plan (2023). The Labour Government also announced several new bills in 2024 relevant to net zero.

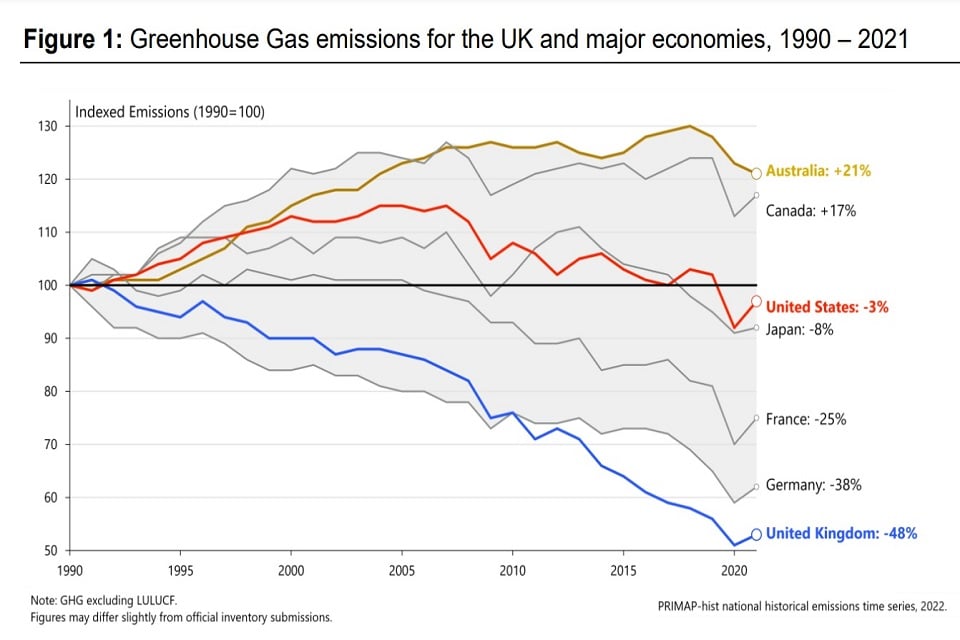

The UK are setting the pace and lead the other G7 countries. Between 1990 and 2021, UK cut net emissions by 48% whilst growing the economy by 65%.

The built environment sector is a significant contributor to carbon emissions, accounting for approximately 25% of the UK’s total output. It is estimated that this jumps to 42% if associated vehicle emissions are counted.

The industry estimates that 80% of UK buildings that will exist in 2050 have already been built—and most are carbon-emitting. This underscores the critical need for retrofitting.

Buzzwords

Short definitions of common language used

Net zero carbon key drivers in the built environment:

Certain sectors are seeing significant growth, with owners, investors and occupiers strategically evaluating assets. Let’s look at the drivers that are creating progress:

- Regulatory Compliance

The UK government are setting stringent energy performance standards, to improve the energy efficiency and reduce carbon emissions. Occupiers are aware and seek buildings that meet or exceed these requirements. The average building stock EPC ratings are poor, varying within regions and sectors. For context, it’s estimated that currently, only 10% of industrial buildings are above the EPC B grade, highlighting the need for improvements.

- Corporate Sustainability Goals

Companies have well developed ESG policies and have set ambitious aspirations with regards to net zero carbon. The industry will need to react to provide properties that align with the objectives.

The Science Based Targets initiative (SBTi) has seen over 7,600 businesses commit to carbon reduction goals.

- Operational Cost Savings

Occupiers are increasingly recognising the financial benefits of energy-efficient buildings. A survey by CBRE found that three-fourths of occupiers would be willing to pay higher rents for properties that offer green energy solutions, citing potential long-term savings on operational costs. This is heightened by the electrification strategy adopted and surging electricity price changes, specifically during the last 5 years.

Electricity demand globally is predicted to increase by 18% by 2030, according to a IEA report.

- Energy Security

The increase demand on electricity, coupled with market growth in large energy consuming markets have left developers and investors concerned about securing power but also the power supply resilience in operation.

Sparked by the pandemic, the industrial and logistics sector has witnessed unprecedented growth, with a trend relying on advanced technologies, robotics, and electric vehicle fleets. Then there is the growth within the life science, advanced manufacturing, and data centre market.

JLL recently published an article on their website that indicated a potential 41% global unmet demand in the industrial sector between 2025 – 2030. In context, JLL summarised

for every two square feet of global demand for low carbon, sustainable industrial and logistics space, less than one square foot is in the pipeline.

The challenges are not going away. The M&E Consultants have long lived with the challenges but have become more recently aware of energy resilience. Adam Selvey recently covered this in a very interesting article in the CIBSE Journal (June 2025 edition), voicing that power-grid congestion could threaten the clean energy transition, voicing the potential to transition from alternating current (AC) to direct current (DC) and microgrids as we advance to a renewable future.

Smart-grid networks, microgrids and self- reliant energy production will help push net zero forward for the major energy consuming sectors.

Key challenges

Different sectors face different challenges. While the UK Net Zero Carbon Buildings Standard adapts targets to suit various building types, both physical and economic obstacles still persist.

Residential landlords face high upfront costs and disruptive work to undertake refurbishments of existing assets. However, over the long term reduced energy costs and improved assets will increase property value.

Public sector buildings, funded by taxpayers, will need the most carefully tailored and patient approach, relying on industry expertise for gradual guidance. It is, at its core, a moral investment.

The demand for low-carbon industrial and logistics properties in the UK is experiencing significant growth. According to the Royal Institution of Chartered Surveyors (RICS), approximately 65% of UK occupiers reported an increase in demand for green and sustainable buildings over the past 12 months. The commercial and industrial sectors capture the key drivers discussed in this blog but also have the largest challenges to overcome.

Another significant challenge sits within the industry. Over the years, a skills gap has been recognised which could threaten the achievement of targets between now and 2050. However, this gap—alongside the moral imperative of the challenge—is also helping to attract new talent.

In engineering alone, we have witnessed graduates considering construction over the typically more financially rewarding industries such as automotive and aerospace. This potential must be actively nurtured, as the construction industry has unfortunately struggled with retaining talent early in their careers. Company initiatives have improved, but grass route apprenticeships that are supported by companies, institutions and education providers need to be strengthened.

Retrofit

Although the industry prefers standardised approaches, we need to be mindful that retrofit projects require tailored flexible pathways to net zero. The industry will heavily rely on the expertise and knowledge of professionals to get this right – innovative technologies and materials alone won’t provide the correct result.

The industry has recognised a skills gap that could threaten the achievement of targets between now and 2050. However, this gap—alongside the moral imperative of the challenge—is also helping to attract new talent.

In engineering alone, we have witnessed graduates considering construction over the typically more financially rewarding industries such as automotive and aerospace. However, this potential must be actively nurtured, as the construction industry has unfortunately struggled with retaining talent early in their careers.

The new build design philosophy is well known and prescribed, in terms of improving a building’s fabric, lowering demand, selecting smart efficient technologies, appropriately applying renewable technology and monitoring.

Retrofit is a little different. Clearly incredibly positive from an embodied carbon perspective but operationally can be tricky. Heritage, disruption, project timescales and financial feasibility all create barriers. The assets need to be carefully assessed, then approximately optimised and enhanced in an effective manner.

With considered design we have seen unlettable buildings turned into functional, high quality, low carbon assets. A notable example was documented in June’s CIBSE Journal. The Cathedral Hill Industrial Estate consisted of a 13 small unit industrial development that was 30 years old. The rental valve was reported as 33% below the average for the Surrey area. After a £10.6m refurbishment, the rental values increased by an impressive 220%. The scheme achieved BREEAM excellent and is on target to achieve net zero whole life.

Design for the future

There is a lot of adversity to overcome to achieve net zero, economically, politically and physically. That said, the UK build environment is demonstrating collective optimism in the face of the challenges.

This was clear at both this year’s MIPIM and UKREiiF events, where tough questions were met with honest responses—most importantly, accompanied by constructive solutions.

Helping to set the pace globally is positive and something to be celebrated. It can provide future skilled workforce opportunities, economic growth, energy security and fit-for-purpose healthy environments. We want to avoid the position when taxation become a blunt lever to force progress.

Brookbanks are extremely passionate about the Built Environment. Carbon reduction is a crucial element for our industry to secure a sustainable future. We hold the expertise and tools to be your consulting partner to drive your carbon reduction aspirations forward.

Brookbanks understands this has become a priority to companies. We are here to navigate the challenges with you, providing project tailored solutions in a practical and proactive manner.

Meet our Mechanical and Engineering Team...

Graduate Mechanical Engineer

Charlotte Rasinsky

Read Profile

Associate Electrical Director

Danny Mills

Read Profile

Director, Mechanical and Electrical Engineering Group

Grant Vasey

Read Profile

Associate Director, Mechanical and Electrical Engineering Group

Jack Kenny

Read Profile

Director, Mechanical and Electrical Engineering Group

Lucy Wildesmith

Read Profile

National Director for Building Engineering / Head of London Office

Paul Rushmer

Read ProfileCheck Out Our Services...

Civil Engineering Group

Cost & Commercial Group

Infrastructure/Abnormal/Site-Wide Cost Planning. We have vast experience in structuring, maintaining and managing budgets of hundreds of million pounds, en...

View More

Development Management Group

We are one of the UK's leading partners to blue chip developers, funders and land promoters. From securing planning consents for major house building schem...

View More

Land, Development and Communities Group

Our Land, Development and Communities Group (LDC) has built an enviable reputation across our industry as leading providers of a variety of services with t...

View More

Mechanical and Electrical Engineering Group

Our Mechanical and Electrical Engineering Group has a renowned team of award-winning, energy-centric building services specialists.

We are a creative te...

View More

Structural Engineering Group

Our Structural Engineering Group can trace its origins back to its formation in 1984. From the outset it quickly gained a reputation for producing practica...

View More

More News

Why Foundation Strategy is a key for Infrastructure Delivery

April 3, 2026

Ground conditions remain one of the biggest sources of cost, carbon and programme risk in infrastructure delivery, yet foundation strategy is still too often considered too late. When layouts and levels are fixed before the ground is understood, projects lose the chance to shape efficient, predictable outcomes. This article explores why early, ground‑led design matters and how treating foundation strategy as a front‑end decision can unlock clarity, reduce risk and improve overall project performance.

Podcast Episode #14: The Housing Crisis, How Did We Get Here?

April 2, 2026

Explore how decades of UK housing policy, supply constraints, planning and affordability pressures created today’s housing crisis, and what lessons the past offers for future delivery.

Our March 2026 Newsletter

March 31, 2026

Welcome to our March 2026 newsletter. In this issue, we’ll tell you more about how we help SMEs prioritise what matters, avoid the common financial traps, and get projects moving, backed by our experienced team who have real housebuilding experience. We’re looking back on our March webinar, where Jack Kenny and Paul Rushmer gave an overview of how to optimise mechanical and electrical designs specifically for high-risk buildings. Plus, we’ll highlight this month’s podcasts! The first explored where structural engineering and building services design overlap, and why good coordination is so important to project delivery. In episode two, Hannah Simpson, Fran Walker, and Isabelle Latuszka spoke about their early-career experiences and how diverse backgrounds add real value to projects. Below, you’ll also get to hear about some exciting awards news and an event we’re co-hosting with the LPDF in Manchester.